Central Bank Independence: Views from History and Machine Learning

How independent are central banks?

Central bank independence is elusive. A central bank’s independence is never absolute; other officials and branches of government regularly dispute and challenge its extent. Moreover, central bank independence is difficult to measure: there exist different metrics of exactly how independent an institution is at a point in time. Finally, central bank independence can and does change. This renders a snapshot of independence a potentially inaccurate picture of the past, present, and future.

In our paper we focus on legal independence, assigning numerical ratings based on our reading the relevant passages of the central bank’s statutes, and extending the analysis back to the beginning of the 19th century. This approach of assigning numerical ratings for various dimensions of legal independence based on language in central bank statutes involves human judgment in interpreting the relevant passages. We therefore compare our findings with results obtained using natural language processing and machine learning techniques. We analyze 90 central bank acts using machine-vector regression and topic modeling, identifying topics that relate positively and negatively to our independence index.

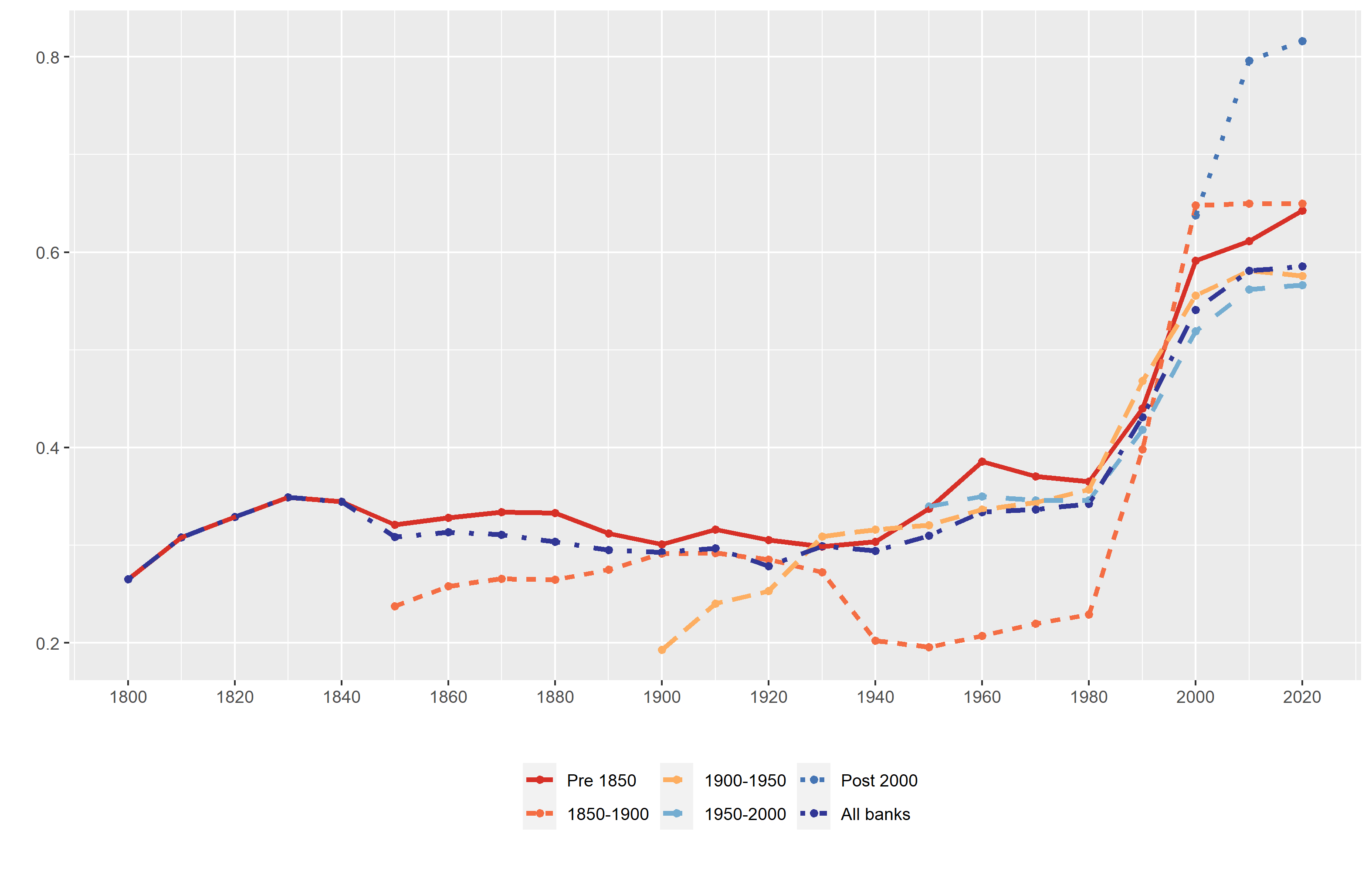

The fact that stands out most clearly from the long-run analysis is the rise in central bank independence since 1980. The extent of the change and the high level of legal independence in this period have no precedent in earlier history. In addition, however, we document a slower ongoing rise in average levels of independence starting in the 1920s. As we show, the increase in the extent of independence in the 1920s and 1930s was associated with the creation of a number of new, relatively independent central banks. We also document a modest but ongoing increase in average levels of independence spanning the four subsequent decades.

Turning to natural language analysis, we find that the topic with the largest positive contribution to explaining variations in central bank independence concerns disclosure, transparency, and reporting obligations. This is consistent with the presumption that independence and accountability go together, and that transparency is a mechanism by which central banks provide information such that they can be held accountable by politicians and the public. The topic with the largest negative contribution has to do with regulatory powers over, inter alia, securities markets. These powers complicate the central bank’s mandate and make accountability more difficult, rendering independence more problematic.

Trends and Fluctuations 1800–2022

The rise in central bank independence since 1980 stands out. Both the extent of the change and the high level of statutory independence in this period have no precedent in earlier history. The sharp rise in central bank independence to levels surpassing those reached previously is common to central banks in existence already in the first half of the 19th century, central banks established in the second half of that century, central banks created in the first half of the 20th century, and central banks founded more recently. What we find does not reflect cohort effects, in other words.

Figure 1: Preferred legal Central Bank independence index (LVAU) by period of central bank establishment

The independence of the central bank governor increases steadily from 1891, as indicated in Figure 2, and unlike other components it does not decline significantly at any point in the subsequent period.

The 1930s and World War II-era decline in independence can be understood as a reaction against poor monetary management in the Great Depression and the fiscal imperatives and finances of war. In the 1920s, the doctrine of central bank independence was spread by the League of Nations, in conjunction with stabilization and institution-building missions in the aftermath of World War I. All this is evident from how the increase in overall independence in this period is driven by the yellow line in Figure 1 depicting central banks newly established in the first half of the 20th century.

We also see an ongoing increase in average levels of independence spanning the four sub- sequent decades. This was driven by modest increases in independence for the same cohort of central banks established in the first half of the 20th century but also for the cohort of central banks established in the 19th century that now saw their transparency enhanced.

Analysis of Components

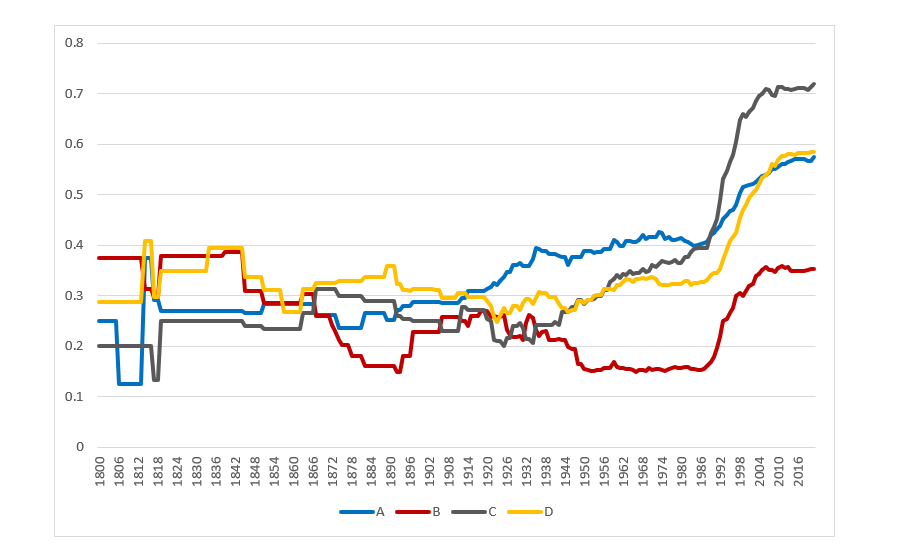

We can also glean insight from the individual components of the independence index obtained by human reader assessment of central bank statutes.

Figure 2: Components of Legal Central Bank Independence indexes 1800-2021

- Component A covers limitations on the CEO: term of office, by whom appointed, provisions for dismissal, simultaneous holding other offices.

The independence of the central bank governor increases steadily from 1891, as indicated in Figure 2, and unlike other components it does not decline significantly at any point in the subsequent period. The scope for dismissing the governor, an important element of CEO independence, was always limited by central bank laws, but additional central bank statutes limited such scope starting in the 1920s.

- Component B is related to policy formulation (PF), covering the role of the central bank in monetary policy formulation, resolution of conflict between the central bank and the government over monetary policy and the role of the central bank in the budget process.

- Component C is provisions on objectives (Obj), including emphasis on price stability versus other goals.

- Component D is limitations on lending to the government: limits regarding the volume, maturity, interest rate and conditions for securitized and non-securitized lending.

How independent are central banks? We dive into a historical analysis using both human reader-based methods and natural text analysis using machine learning to assess central bank independence.